Viewpoints

In this issue of Viewpoints: America at 250, Beyond the Map

As Americans gather this Independence Day, this year’s celebration carries special significance. On July 4, 2026, our nation marks its 250th birthday, a remarkable milestone for an experiment in self-government that began with little certainty and considerable risk.

When we reflect on American history, it is tempting to focus solely on the outcome. The United States ultimately became one of - if not - the greatest economic and military powers in the history of civilization. Along the way, however, we endured wars, depressions, political turmoil, and perpetual social change. We produced innovations that transformed the world and altered the course of human progress.

Yet history rarely feels inevitable while it is being lived.

Looking backward, America’s rise can appear almost preordained. Looking forward from any point along the journey, however, the path was often unclear, the obstacles daunting, and success far from guaranteed.

Few episodes illustrate this reality better than the expedition undertaken by Meriwether Lewis and William Clark in 1804 - a uniquely American story of courage, exploration, and perseverance.

Charged with exploring the vast territory acquired through the Louisiana Purchase, Lewis and Clark ventured into a wilderness that existed largely as blank space on the map. They faced rugged terrain, harsh weather, unfamiliar cultures, disease, and even American’s first encounter with Grizzly Bears. Despite these challenges, they learned, adapted and ultimately accomplished what many considered impossible. Reflecting on their journey, a simple observation is striking: Lewis and Clark did not succeed because they knew exactly what lay ahead. They succeeded because they had the courage to enter the unknown, the discipline to adapt when reality differed from expectation, and the conviction to keep moving toward their North Star.

In many ways, that is the American story: moving forward into uncertainty while remaining anchored to the principles that give the journey purpose.

The Challenge of Uncertainty

One of history’s great tricks is that uncertainty tends to disappear in hindsight.

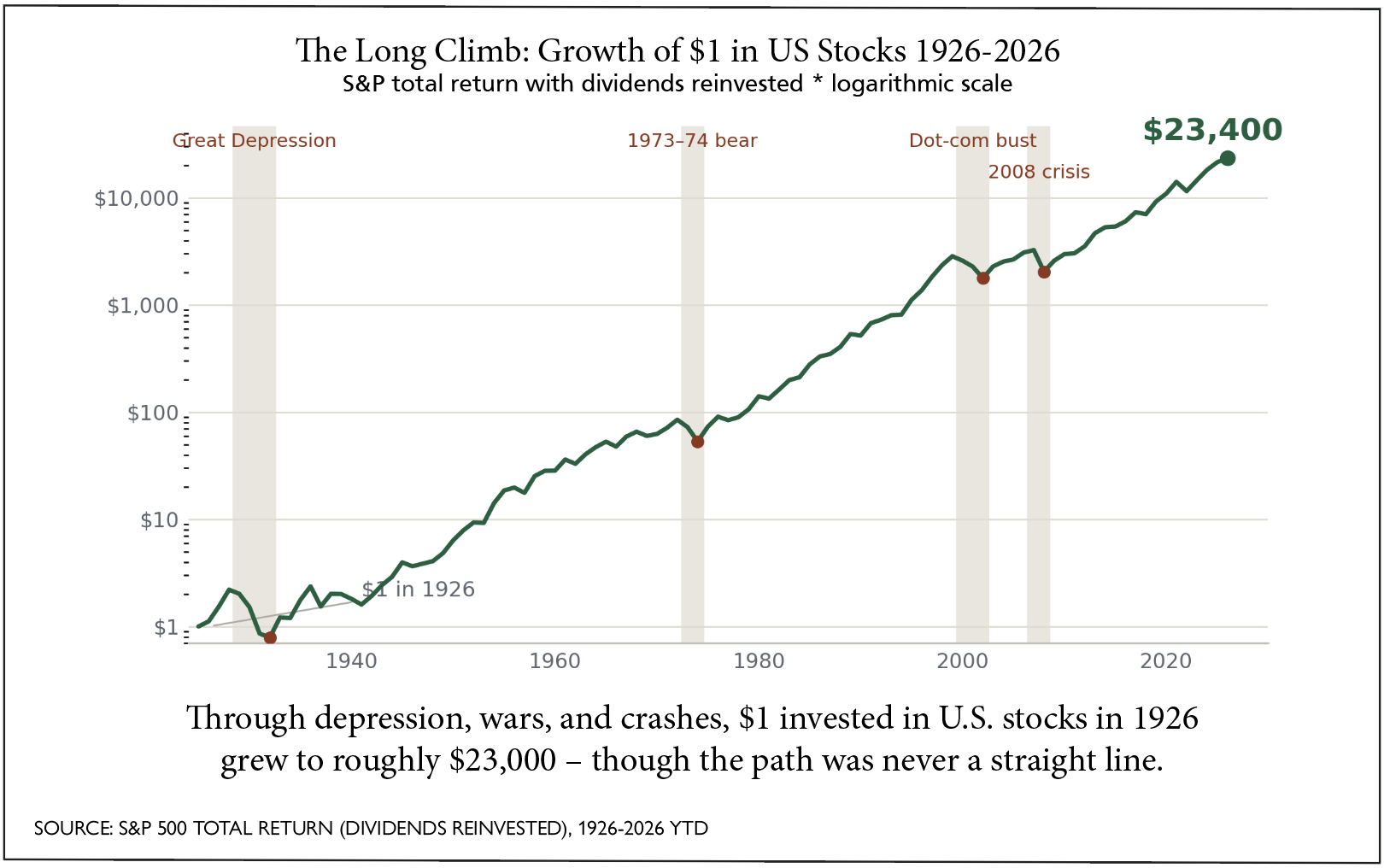

Today, with the benefit of hindsight, we know how many of these stories ended: Lewis and Clark reached the Pacific Ocean, the Union survived the Civil War, the nation emerged from the Great Depression, victory was achieved in World War II, and the economy recovered from financial crises, recessions, and countless other periods of disruption.

But the people living through those moments knew none of those things.

Every generation encounters reasons to believe its challenges are uniquely daunting. Yet while the details change, the rhythm of history often feels familiar. Time and again, resilience, adaptability, and innovation have revealed paths forward that were not visible at the outset.

That lesson feels particularly relevant today. A generation of college graduates is entering the workforce wondering how artificial intelligence may reshape the careers they hoped to pursue. Business leaders are being forced to reconsider how work gets done. Investors are grappling with questions surrounding technological disruption, government debt, geopolitics, inflation, and the future shape of the global economy.

These concerns are understandable, but uncertainty itself is not new. In fact, uncertainty has been the constant companion of nearly every meaningful advance in human history.

Forging Our Own Path

As SG & Co. approaches its fiftieth year serving clients, this lesson resonates deeply with us.

The responsibility of stewardship extends beyond preserving what has been built; it also requires preparing thoughtfully for what comes next. Financial markets, technology, and client needs will inevitably evolve, and enduring organizations are those capable of honoring the principles that shaped them while remaining adaptable enough to navigate change.

That balance feels especially important in today’s environment. We find ourselves in a market that appears historically expensive by many traditional measures, while recognizing many of the forces that led markets over the last decade may not necessarily define the next. Stock market leadership of the coming years is likely to look very different from the leadership of the years just passed. In such an environment, discipline becomes even more important.

Like any worthwhile journey, the path forward is not fully mapped, nor should we expect it to be.

What gives us confidence is not the illusion of certainty, but the knowledge that sound principles, disciplined decision-making, and a willingness to adapt have served our clients well across generations of challenges.

Lewis and Clark adapted constantly throughout their journey, but their mission never changed. Likewise, while markets, technologies, and economic conditions evolve, our investment compass remains firmly rooted in the principles that have guided the firm for nearly five decades: discipline, patience, ownership of high-quality businesses, and a focus on growing streams of dividend income.

The tools may change. The landscape may change. The challenges certainly will.

Our North Star remains the same.

Looking Beyond the Horizon

As America begins its next 250 years, perhaps the most important lesson from the first 250 is that progress rarely comes from waiting for certainty.

The individuals who built this nation did not possess perfect information. They possessed conviction. They adapted when circumstances changed, remained grounded in enduring principles, and moved forward despite uncertainty.

Lewis and Clark exemplified that spirit. So, too, did the countless Americans who followed them.

The future, as it always has been, remains unwritten. Yet history offers good reason for optimism. Time and again, Americans have demonstrated an extraordinary capacity to adapt to changing circumstances while remaining true to the principles that guide them.

At SG & Co., we intend to do the same.

Michael P. Moeller, CIMA®

Portfolio Manager & Director of Research